The Rise of Intelligent Tourism Ecosystems

The era of cost-optimized globalization is giving way to one driven by sovereignty, resilient supply chains and control over critical technologies. Industrial policy is no longer a marginal tool: it has become a central lever of power, competitiveness and decarbonization.

For three decades, advanced economies largely relied on open markets, specialization and global value chains to allocate production efficiently. That model is now under pressure. Supply chain shocks, geopolitical tensions, the clean-tech race and the rise of Asia have all made one fact impossible to ignore: technological leadership does not rest on research alone. It depends on the ability to control the full chain - from design and financing to industrialization and scale-up.

This is the core message of Sia’s study on industrial policy. The report shows that industrial policy has returned because governments increasingly view manufacturing capacity, technological depth and supply-chain control as strategic assets. In that sense, industrial policy is no longer only about economics: it also speaks to national security, energy transition, employment, trade and long-term resilience.

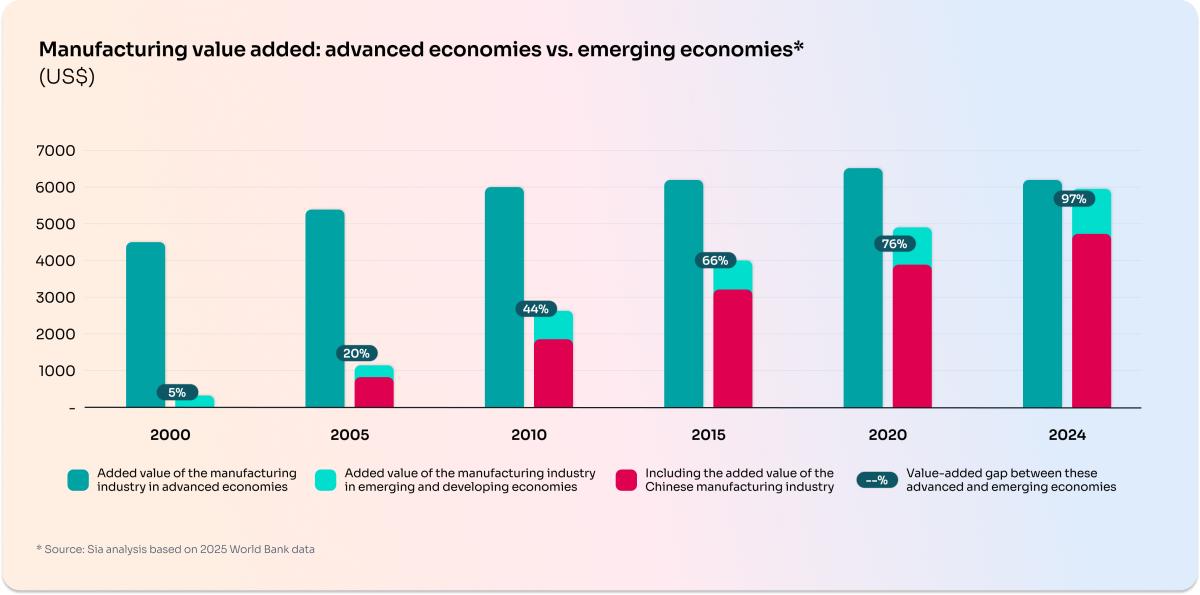

One of the report’s strongest findings is the extent of the manufacturing catch-up achieved by emerging Asian economies. In 2000, the manufacturing value added of emerging and developing Asian economies represented only about 5% of that of advanced economies. By 2024, that figure had reached 97%. In parallel, the share of manufacturing in GDP has eroded across many advanced economies, including the United States, the United Kingdom and Canada.

This trend matters because it changes the geography of power. When production capabilities weaken, countries do not only lose factories - they also lose know-how, supplier ecosystems, execution capabilities and, eventually, influence over future technology trajectories. Industrial policy is therefore returning as a response to a real strategic vulnerability, not simply as an ideological shift.

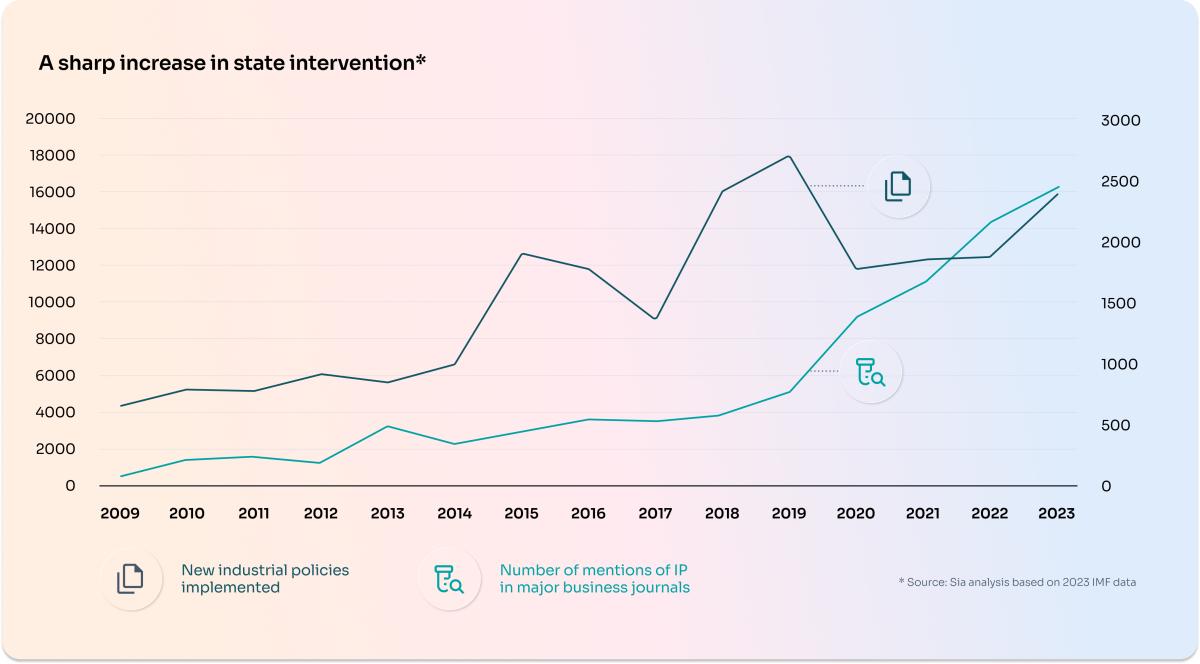

The study also highlights how quickly public intervention has intensified. Industrial policy measures more than doubled within three years, with over 2,500 industrial policies identified in 2023. This acceleration reflects at least three structural forces: the need to secure supply chains after successive crises, the ambition to capture the value of the energy transition, and the renewed role of the state in de-risking strategic sectors where private capital alone is not sufficient.

Another important dynamic is reciprocity. Once one major bloc subsidizes a strategic sector, others tend to respond. This “tit-for-tat” logic fuels an escalating global competition around semiconductors, critical minerals, batteries, hydrogen, solar technologies and other strategic value chains.

Industrial policy is not a single instrument. The report shows a clear contrast between advanced economies and emerging economies. Advanced economies rely more heavily on financial and fiscal tools such as direct subsidies, public loans and tax relief. Emerging economies, by contrast, make greater use of trade and localization instruments, including tariffs, import taxation and local-content requirements. This reflects different strategic positions: preserving leadership for the former, building industrial depth and catching up for the latter.

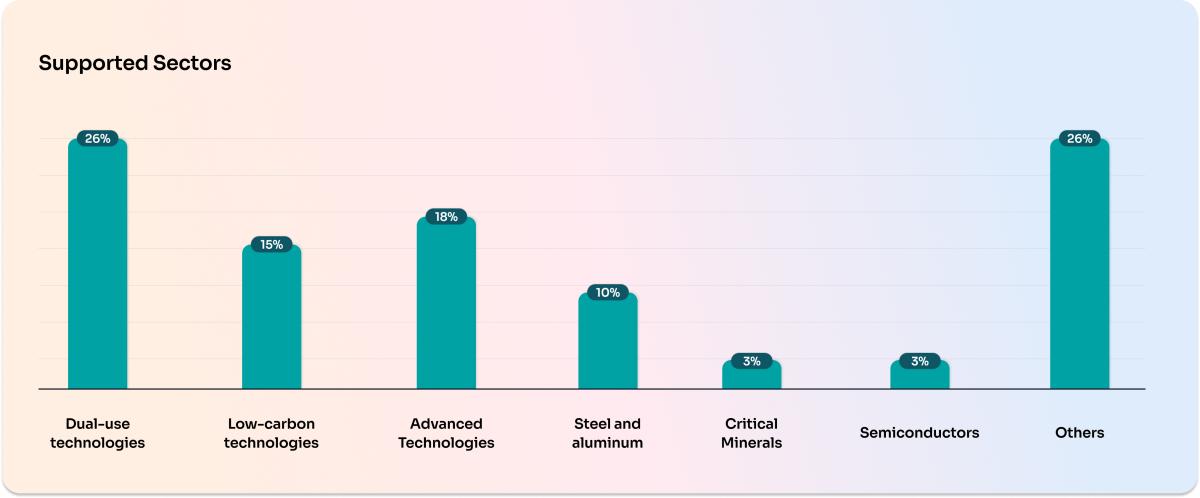

In terms of sectors, support is concentrated on a limited set of high-value and strategically sensitive activities. The study identifies low-carbon technologies, dual-use civil/military applications and advanced technologies as the leading categories, with steel, aluminum, critical minerals and semiconductors also appearing as targeted areas. In other words, industrial policy is being used where power, resilience and future growth intersect.

A major strength of the study is that it does not present industrial policy as a miracle solution. Instead, it shows that it is an inherently ambivalent instrument. On the one hand, industrial policy can reduce critical dependencies, support strategic value chains, lower the green premium of emerging clean technologies and rebuild skilled employment in deindustrialized regions. On the other hand, it can distort competition, trigger subsidy races, create rent-seeking behaviour, overburden public finances and back technologies that never reach scale.

The lesson is straightforward: industrial policy only works when objectives are clear, governance is disciplined, and the state is able to combine long-term direction with credible performance criteria. The study illustrates this balance through contrasted examples — from the success of Airbus or the French nuclear build-out to the failure of Europe to preserve a competitive solar manufacturing base in the face of Chinese scale and coordination.

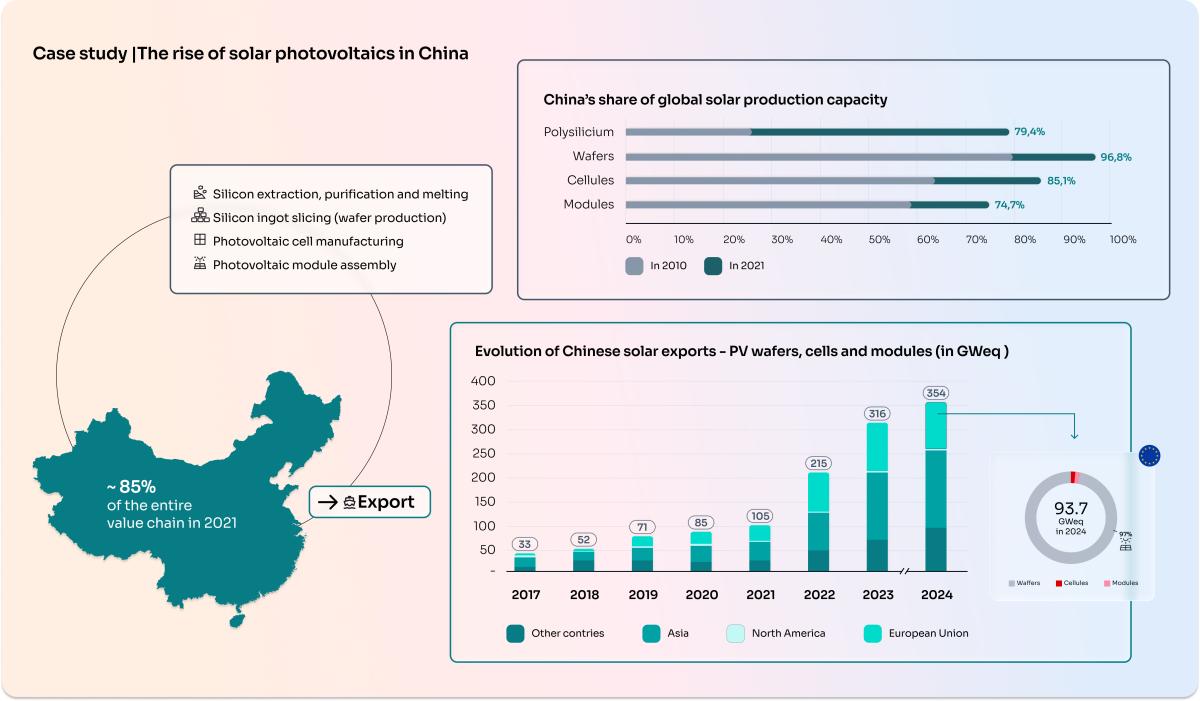

The photovoltaic case study is especially instructive. According to the report, China moved from early technological dependence to overwhelming industrial dominance through a coherent, long-term and highly coordinated strategy. Successive five-year plans identified solar as a strategic sector, public funding supported R&D and scale-up, local governments competed to attract investment, and the policy framework evolved from emergence to consolidation and then dominance.

By 2021, China accounted for roughly 85% of global production capacity across the solar value chain, with particularly strong positions in polysilicon, wafers, cells and modules. At the same time, rising production capacity translated into a powerful export engine. By 2024, Chinese exports of wafers, cells and modules had reached 354 GWeq, making China the pivotal supplier to international solar markets. This is a textbook example of industrial policy moving all the way from policy intent to factory-level execution.

Managing Partner | Brussels

Jean is Managing Partner and Climate Analysis Global Lead at Sia Partners. In charge of several business units for global transformations related to Sustainability and low Carbon strategies, AI/DS, Risk, Pricing & Revenues Mgt, Innovation & Strategic Roadmap.

Managing Director, Energy & Environment, Utilities, Transports and Manufacturing | Montréal

Myrielle, an experienced Managing Director, advises on strategic climate solutions for various North American private and public entities. She has cultivated her expertise around promoting energy efficiency, renewable energy and decarbonization for sustainability goals.