The Rise of Intelligent Tourism Ecosystems

The 2025 edition of the Canadian Hydrogen Observatory highlights Canada’s progress in developing a low-carbon hydrogen sector, analyzing the projects, investments, and resources required to support its transition toward global leadership in clean hydrogen production.

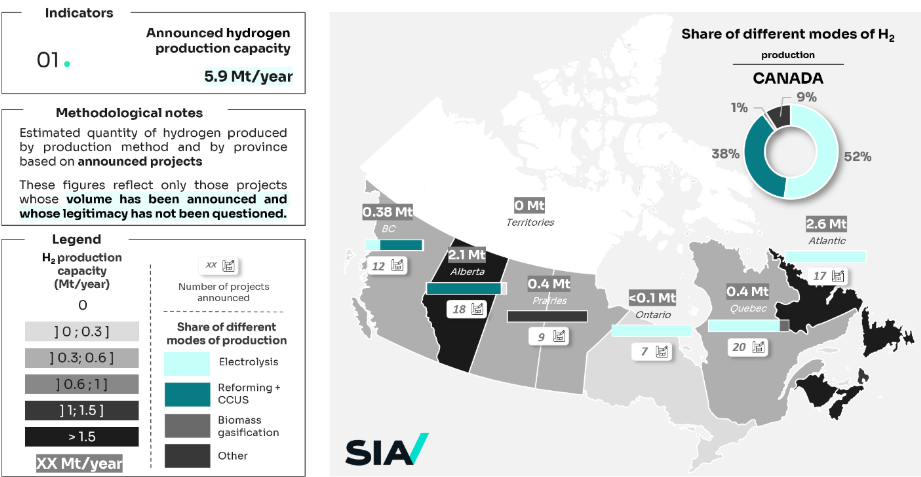

With 103 announced projects and 5.9 Mt of projected hydrogen (H2) production capacity, Canada is continuing its trajectory toward becoming a major global producer of low-carbon H2, dedicated to the decarbonization of no-regret sectors: ammonia and synthetic fuel production, steel, petrochemicals, and heavy-duty mobility.

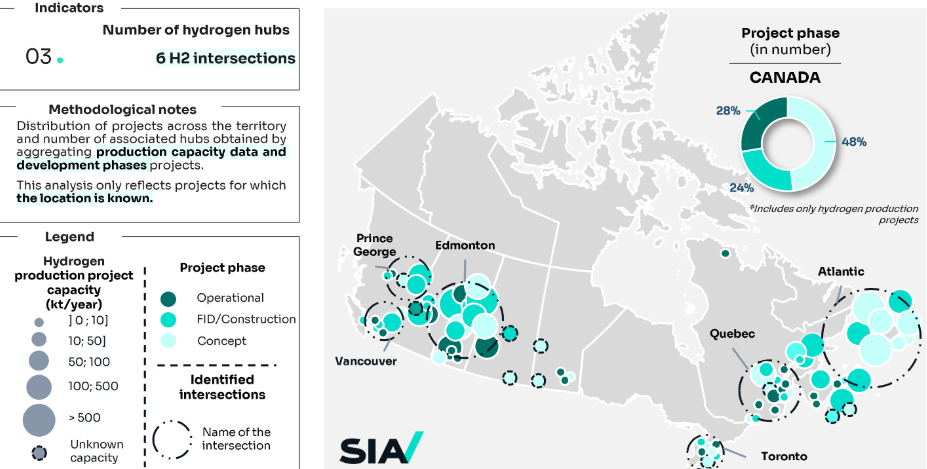

Low-carbon H2 production projects continue to take shape across Canada, with 6 H2 hubs now identified: Prince George and Vancouver in British Columbia, Edmonton in Alberta, southern Ontario, Quebec, and the Atlantic provinces. These regional ecosystems concentrate most projects and provide a response to the energy transition challenges of hard-to-electrify sectors. More than 75% of end-uses are directed toward synthetic fuel production, mostly ammonia intended for export – to Europe from the east of the country, and to Japan from the west. The remaining 25% is split between steel, petrochemicals, and, on a smaller scale, mobility.

The sector is supported by a regulatory framework that has been clarified since 2024, notably with the adoption in June 2024 of the Clean Hydrogen Investment Tax Credit (CH-ITC), which covers 15 to 40% of eligible costs depending on the carbon intensity of the production process. Together, the four investment tax credits (clean hydrogen, carbon capture, utilization and storage; clean electricity; and clean technology manufacturing) would represent approximately C$93 billion in federal subsidies by 2034-2035.

Thanks to Canada's territorial advantages – available land, decarbonized and competitive electricity, strategic port access – the H2 dynamic remains promising. However, due to a lack of visibility and reliable data on the actual evolution of projects, it remains complex to navigate the sector and anticipate its next steps.

This second edition of the Canadian Hydrogen Observatory offers a detailed analysis of the 103 projects identified in Canada, their associated end-uses, and the resources to mobilize to scale up. It now enables – in comparison with the 2024 edition – year-over-year tracking of developments and identification of the factors that allow projects to move forward… or that hold them back.

Since 2024, the number of announced H2 projects has increased slightly (+9), while the total production of these projects has risen from 5.36 to 5.87 Mt. This evolution mainly results from upward adjustments and requalifications of the ambitions of existing projects, offsetting 2 significant abandonments (220 kt) and several schedule delays or adjustments (2.2 Mt). New projects, although numerous, contribute little in volume (60 kt): the announced growth relies above all on the consolidation of projects already underway.

At the global level, the sector is experiencing, for the first time, a downward revision of its announcements (from 49 to 37 Mt/year according to the International Energy Agency), reflecting a natural recalibration after the initial phase of euphoria. Paradoxically, this decline coincides with an improvement in project maturity: approximately 9% of the global pipeline has now reached Final Investment Decision (FID), up nearly 20% compared to 2024.

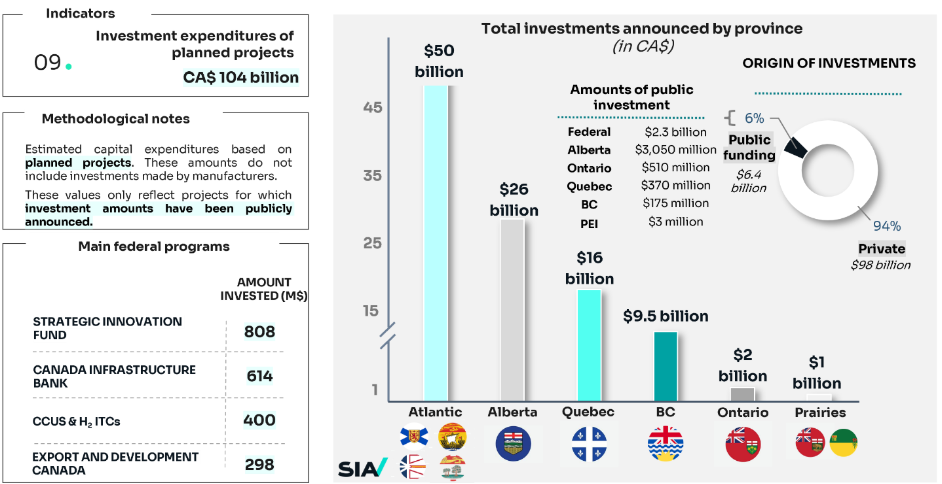

Announced investments in hydrogen projects reach C$104 billion in 2025, approximately 3% of Canadian GDP, compared to C$90 billion in 2024. This 16% growth over one year, driven primarily by Alberta and the Atlantic provinces, reflects above all the refinement of CAPEX for existing projects rather than a multiplication of new investments.

Announced financing remains dominated by the private sector (94%), complemented by targeted public support (6%) coming mostly from the provinces, while significant federal investments are currently being deployed. A strong signal of the de-risking role of public support: of the 4 projects abandoned between 2024 and 2025, none benefited from public support; conversely, 12 of the 17 projects that received public aid still experienced delays, highlighting the complexity of business models even when financing is secured.

The realization of all mapped projects would require 179 TWh of low-carbon electricity per year – i.e., 33% of Canada's current renewable and nuclear production capacity –, 155 hm³ of water, 20.6 GW of electrolyzers, and 71,800 t of critical minerals. These needs highlight the importance of coordinated resource planning, particularly for access to energy blocks – which has already led to the abandonment of several projects such as Coyote in British Columbia and Teal Chimie & Énergie in Quebec – and for securing critical mineral value chains in a tense geopolitical context (notably the Chinese export licenses on scandium and yttrium introduced in April 2025).

Of the 20.6 GW of electrolyzers required, approximately 75% do not yet have an identified technology supplier: a major opportunity for the establishment of manufacturers in Canada and for building a long-term industrial policy. Concretizing these projects would also position Canada as a key exporter, with an estimated impact of C$26.3 billion on the trade balance, mainly via ammonia (green to Europe from the Atlantic provinces, blue to Asia from the west), low-carbon steel, and synthetic methanol.

Managing Director, Energy & Environment, Utilities, Transports and Manufacturing | Montréal

Myrielle, an experienced Managing Director, advises on strategic climate solutions for various North American private and public entities. She has cultivated her expertise around promoting energy efficiency, renewable energy and decarbonization for sustainability goals.