The Rise of Intelligent Tourism Ecosystems

A strategic lever for decarbonization and energy security

Across Europe, biomethane has shifted from a niche solution to a strategic pillar of the energy transition. With more than 1,500 plants and 60 TWh (6.1 bcm) of production capacity reached in 2024, the market is showing sustained growth. The European Commission’s target of 35 bcm (342 TWh) by 2030 implies sharp acceleration in growth. Achieving this ambition demands not only massive investment, but also robust long-term commercial frameworks. Biomethane Purchase Agreements (BPAs) are emerging as one of the instruments to accelerate biomethane development while giving customers access to low-carbon gas.

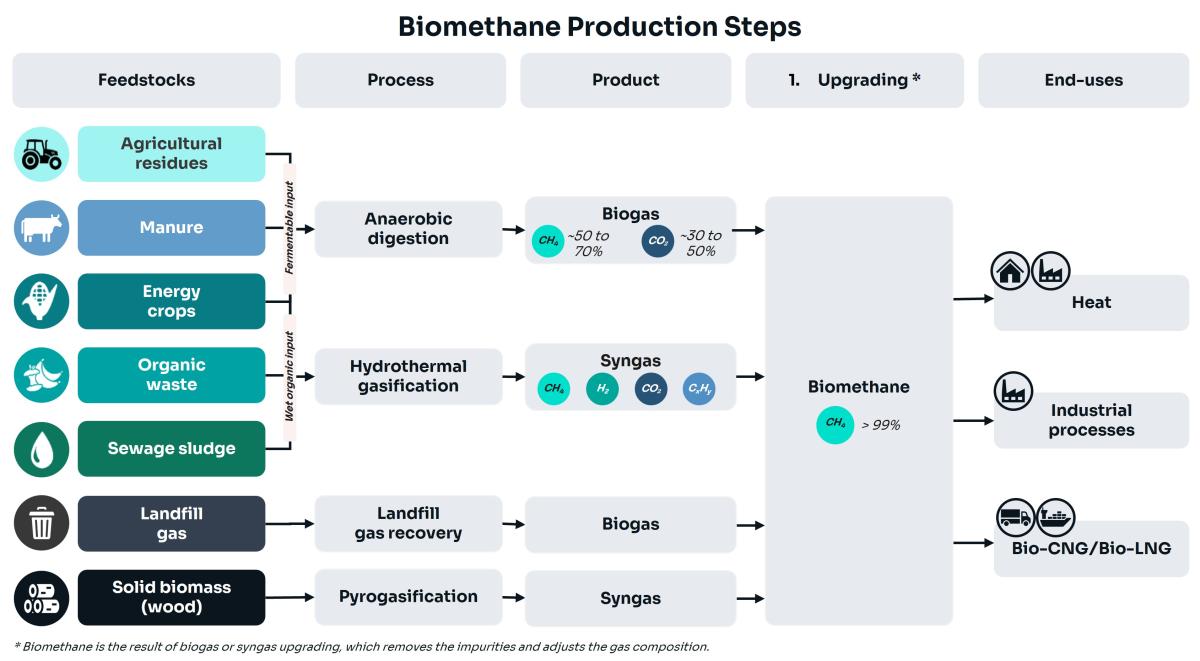

Biomethane is a purified form of biogas produced from the breakdown of organic matter, such as agricultural residues, manure, sewage sludge, organic waste and landfill gas.

Biomethane is fully compatible with the existing gas grid and customers' installations. Biomethane can be used for residential and industrial heating, in industrial processes, or for road and maritime transport in the form of bio-CNG and bio-LNG. Biogenic CO₂ generated as a by-product increasingly opens additional value streams in e-fuels, agri-food and chemicals sectors.

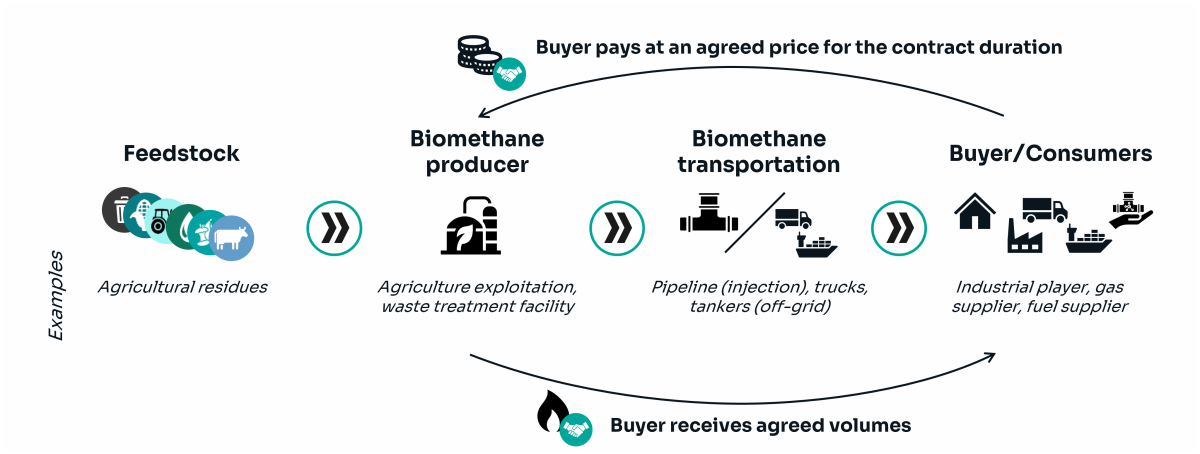

A Biomethane Purchase Agreement is a long-term contract between a biomethane producer and a buyer that typically defines:

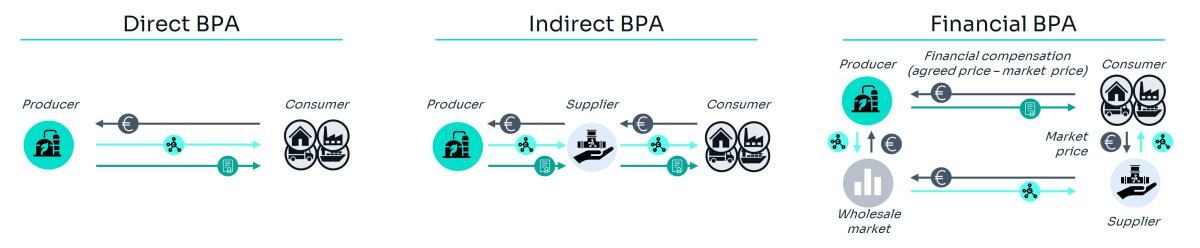

Overall, three main delivery models exist:

Biomethane pricing under each of these BPA delivery model typically reflects three components: production, transport and distribution, and certificates.

Production costs vary broadly depending on the technology deployed, plant size, feedstock type, applicable support mechanisms, and whether the facility is a greenfield or brownfield project.

CAPEX typically represents the largest share of total production costs, making economies of scale a key determinant of competitiveness. OPEX drivers also vary by plant size: smaller facilities tend to be driven by pre-treatment and maintenance, while larger plants are more influenced by labour and additives. Feedstock costs can either be a net expense or a revenue stream, depending on the setup; for example, facilities processing municipal waste or wastewater sludge may earn gate fees, resulting in negative net feedstock costs.

Industrial, utility, and transport players that want to secure green gas for the longer term can enter a BPA and unlock multiple sources of value:

However, the market is still maturing, which requires BPAs to be carefully structured. Several risks must be considered. These include production variability, evolving regulatory frameworks and support schemes, and price exposure if contracts are not aligned with market fundamentals. In addition, quality risks may arise if gas specifications are not clearly defined and properly monitored.

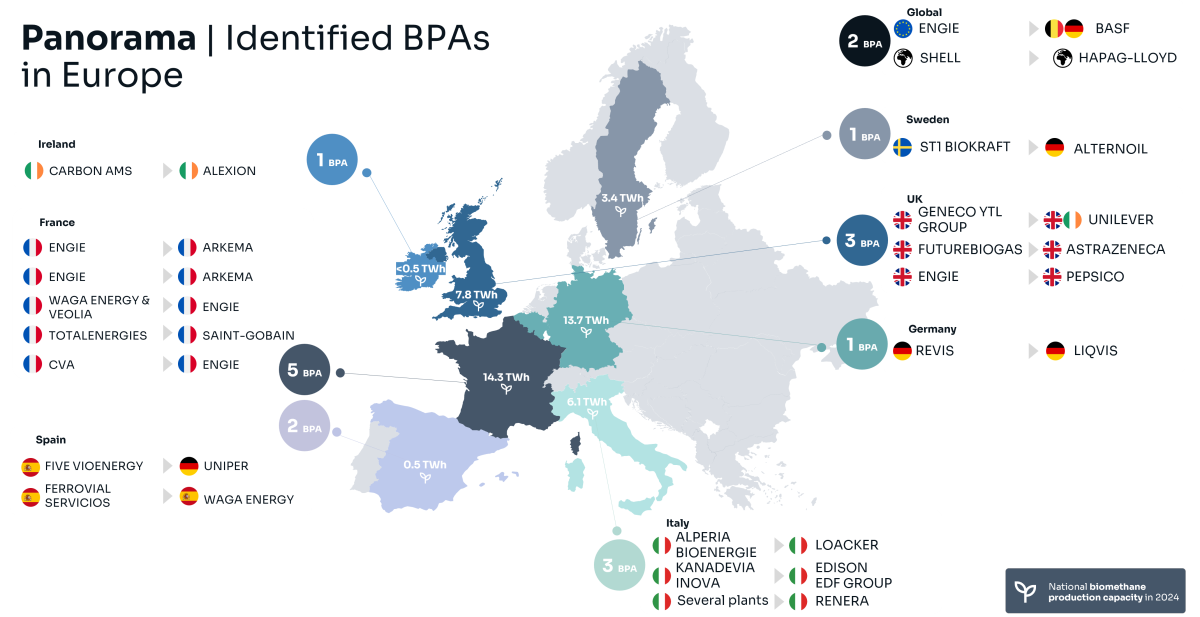

More than 21 TWh (2.1 bcm) had been contracted through BPAs based on publicly disclosed information by April 2026, cumulated over the full duration of the contracts. More than 20 contracted BPAs across Europe that are publicly known.[PT1]

Contract durations range from 3 to 15 years, while annual volumes vary from 10 GWh to 400 GWh, reflecting the diverse needs of contracting companies.

Most agreements have been signed by industrial players, but the transport sector—both road and maritime—as well as gas suppliers seeking to green their offerings, are also increasingly active.

Managing Partner | Brussels

Jean is Managing Partner and Climate Analysis Global Lead at Sia Partners. In charge of several business units for global transformations related to Sustainability and low Carbon strategies, AI/DS, Risk, Pricing & Revenues Mgt, Innovation & Strategic Roadmap.

Managing Director | Paris, France

Stéphanie is a Managing Director based in Paris, specializing in digital transformation, project management, and change management in the energy and utilities sector. She helps organizations optimize processes, enhance CRM, and drive agile transformation initiatives.

Partner Energy | Paris

Sebastien is a Partner in the Energy practice based in Paris. He brings with him more than 25 years of experience in the energy sector, with strong expertise across the entire energy value chain, and a focus on market analysis, strategic positioning, and regulatory frameworks.